Markets

Markets | October 2024 Quarterly Markets Overview & Outlook Economy

John Merrill, Tom Bruce, Curtis Holden, CFA®, October 2, 2024

OVERVIEW.

Over the past quarter, the anticipation of falling interest rates in the U.S. had an outsized impact on financial markets, driving nearly all asset classes higher. Real estate, global infrastructure, and gold were the biggest winners, all posting very strong gains.

All the major asset class performances for the third quarter are shown in Table 1. All returns are total returns which include reinvested dividends and interest.

Source: Morningstar

DOMESTIC STOCKS.

The stock market proved resilient in the third quarter. Despite stretches of elevated volatility, all major U.S. stock averages (except the Russell Small Cap index) reached new all-time highs near quarter end.

U.S. public companies as a whole are performing very well. Both revenues and profit margins reached record highs this past quarter. Thus earnings continued to rise and are now up approximately 10% in 2024. This provides fundamental support to rising stock prices.

Stock buybacks have been another powerful driver of this bull market. See Chart 1. When profitable companies generate extra cash, they often buy back their own shares. With fewer shares available, earnings are higher per share.

This boosts Earnings Per Share (EPS) from which stock price multiples are derived. As pointed out in a prior Newsletter, buybacks have been the single largest source of market liquidity since 2000!

Source: The Wall Street Journal, Goldman Sachs Global Investment Research

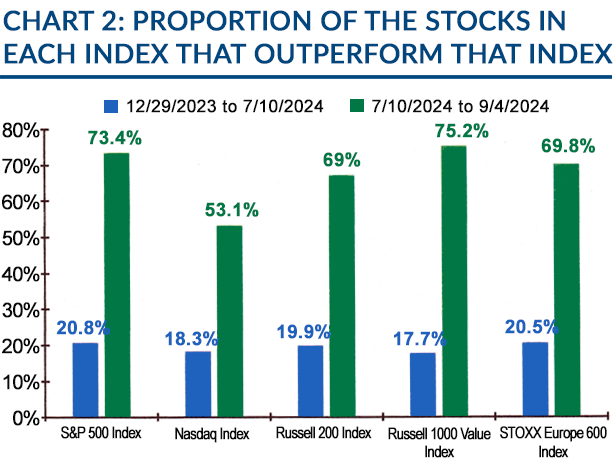

The third quarter also saw the market broaden out as more stocks participated in the rally. The dramatic nature of this change can be seen in Chart 2. From January 1st to July 10th of this year, less than 21% of the stocks in each index shown outperformed that index (blue bars). However, from July 10th through September 4th, about 70% (on average) outperformed (green bars)!

Large cap tech stocks (led by the Magnificent 7) were the big winner in the first half of the year with blowout earnings. Recently though, a wider range of companies have had strong earnings, so the earnings gap has narrowed. See Chart 3.

Source: The Wall Street Journal, Paulsen Perspectives

Small cap stocks enjoyed the greatest gains in their share price in third quarter. This is partly because smaller companies rely more on debt, thus falling interest rates directly helps. In addition, small cap stocks had lagged badly over the past three years and investors were drawn to their lower valuations. Maintaining this performance will require better earnings growth.

INTERNATIONAL STOCKS.

The index of Total International Stocks outperformed the S&P 500 in the third quarter, driven primarily by two key factors.

First, the U.S. Dollar's weakening over the past quarter significantly boosted international stock performance as strong foreign currencies translated into higher Dollar values.

Second, many international companies are mature, dividend-paying firms that perform better in lower interest rate environments. As bond yields decline, these stocks become more attractive to investors seeking income. Historically, they are also very cheap relative to the S&P 500.

However, over the whole period since the Financial Crisis, international stocks have significantly underperformed their U.S. counterparts. See Chart 4.

European stocks, for example, have struggled due to long-term structural challenges discussed in the Economy section. Europe will need to improve its competitiveness with the U.S. if its stock markets are to close the performance gap.

Asian stocks have made steady progress since the end of 2022 despite the major drag from its largest component, China. With the addition of China’s bazooka stimulus at the end of the quarter, Asian stocks should be a prime beneficiary.

Source: The Wall Street Journal, LSEG I/B/E/S, MRB Partners

Emerging markets also outperformed the S&P 500 in the third quarter, as investors reacted to China’s new stimulus measures. While the broader issue is that China continues to move away from a free-market economy (see also page 10), the impact of their stimulus on the global economy – particularly emerging markets – will likely jump start their growth.

How far and how long China’s stimulus programs will go remains uncertain. U.S. stocks have outperformed international stocks over recent years because of better management and a better economic backdrop. U.S. stocks will likely continue to outperform longer term until this basic backdrop changes.

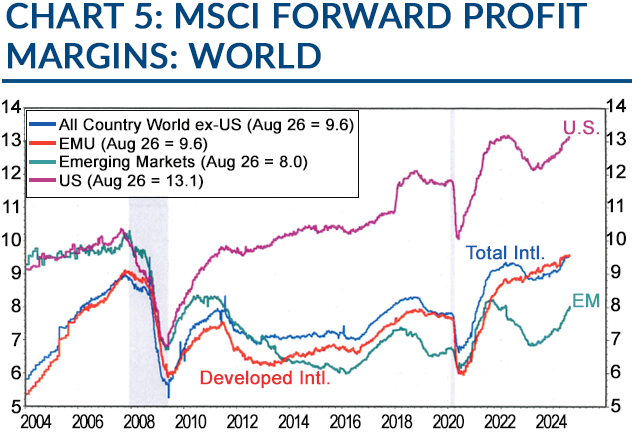

International corporate managements will have to develop higher sustainable profit margins (See Chart 5) if they are to compete with U.S. counterparts.

BONDS.

High quality U.S. bonds delivered a strong performance this quarter, approaching that of the S&P 500. This strength was driven by investors anticipating that the Fed would begin easing interest rates soon and thus driving bonds yields down (prices go up when yields go down).

One of the fascinating aspects of financial markets is how they often price in future events well before they happen. Most are aware that when the Fed cuts interest rates, bond yields typically decline to mirror the lower rate. However, fewer realize that bond yields often drop well in advance, simply based on expectations of a rate cut.

Long-term bond yields declined by a full percentage point, from roughly 4.6% on the 10-year Treasury bond to almost 3.6% well before the Fed’s first rate cut. Interestingly, after the rate cut on September 18th, the yield on the 10-year actually rose and closed the quarter at 3.80%.

The Fed now indicates that its target for the Federal Funds Rate (FFR) at the end of 2025 is 2.88%. This raises the question of what is the appropriate yield for the 10-year Treasury bond to encourage investors to lock up a yield for those 10 years? Historically, the answer would be around 4.5%. From this perspective, longer term U.S. Treasury bonds appear fully valued unless a recession or financial accident causes the Fed to drop the FFR much more than they now anticipate.

REAL ASSETS.

REITs and other yield sensitive equities emerged as the top performers this quarter. For REITs, the drop in bond yields brought down interest rates on commercial real estate loans, offering a much-needed lifeline to real estate investors. Global infrastructure was the next best performer, as their higher dividend payouts compare favorably to lower bond yields.

In contrast to real estate and infrastructure, commodities struggled. Commodities thrive in periods of strong global growth. While the U.S. economy has remained strong, slower growth in other regions, particularly China, has weighed on the commodity sector. That may now change with China’s new stimulus programs.

Oil prices have also declined recently, pressured by a combination of relatively soft global growth and strong increases in available non-OPEC supply.

GOLD.

Gold has been the standout performer of 2024, reaching new record highs and showing no signs of slowing down. It has also bested the S&P 500 for the past one-, three-, and five-year periods.

Several factors have contributed to gold's impressive run. As the Fed engineers lower interest rates, gold should benefit. Lower interest rates reduce the opportunity cost of holding non-yielding assets like gold, making it more attractive to investors.

Additionally, rising geopolitical tensions have further boosted gold's appeal as a safe-haven asset. In times of uncertainty, investors often flock to gold for its stability. However, a new dynamic is the rise of authoritarian regimes that are searching for alternatives to the Dollar.

Source: Tanglewood Total Wealth Management

Source: The Wall Street Journal, LSEG Datastream and Yardeni Research