Markets

Markets | August 2024 Market Update

John Merrill, Brian Merrill, Curtis Holden, Tom Bruce, August 2024

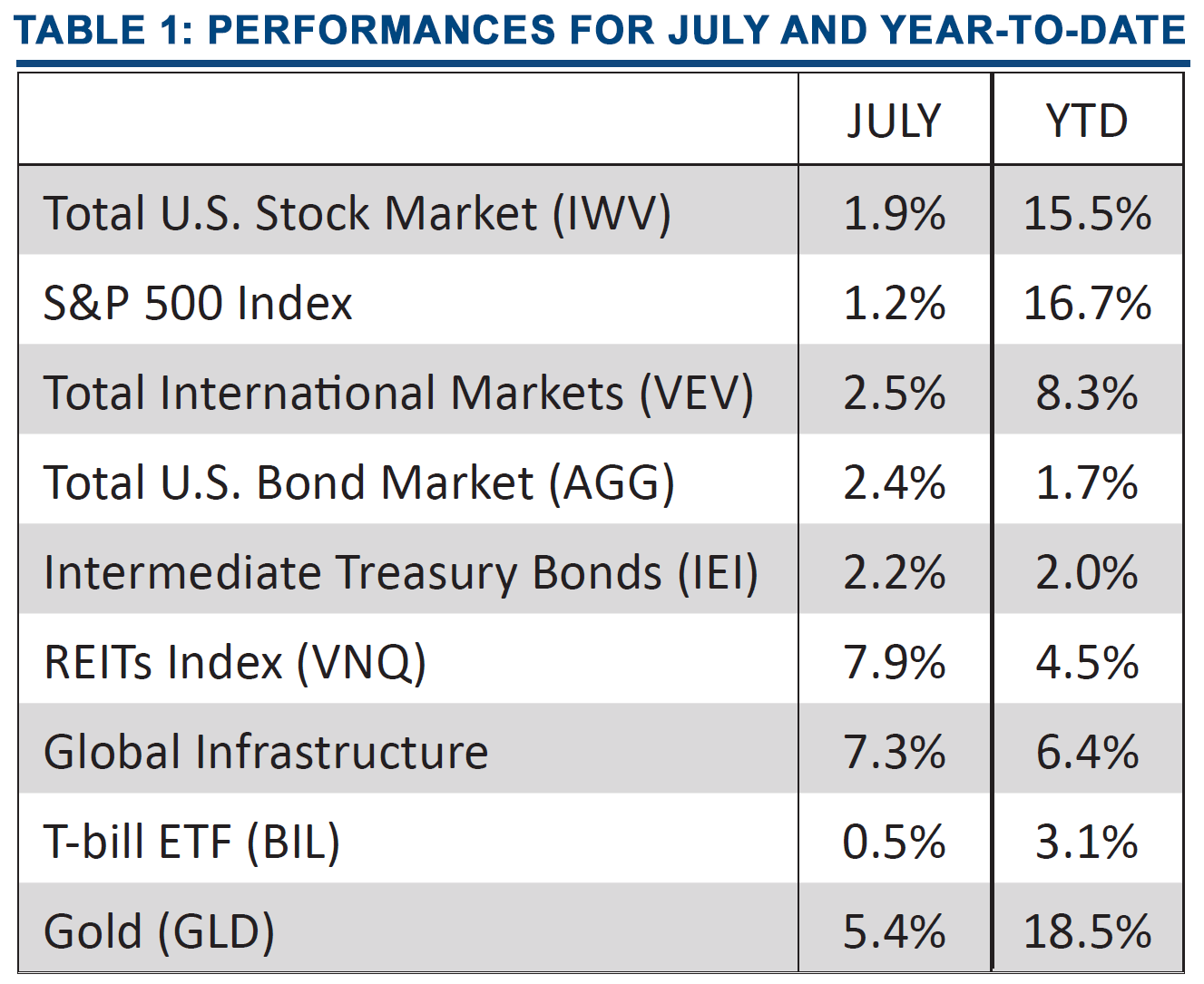

MARKETS. The major equity asset classes, both domestic and international, produced modest gains in July despite the major daily gyrations. The interest sensitive asset classes including Bonds, REITs, and infrastructure posted relatively large gains. See Table 1.

Source: Y-charts

Domestic Stocks. July began as a quiet month, with a continuation of the themes that have propelled markets all year with the Magnificent 7 outperforming.

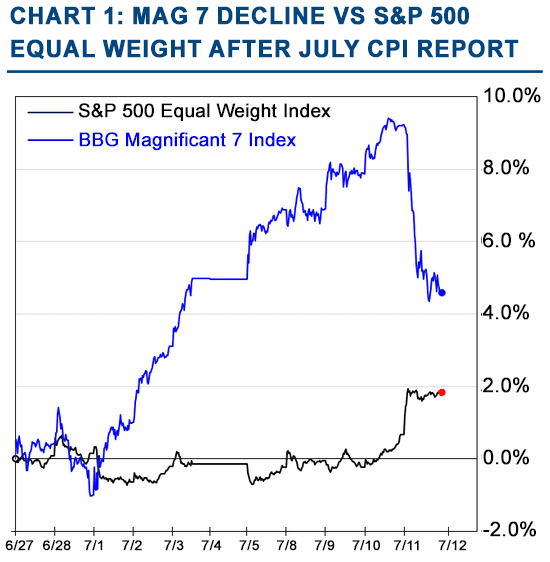

This all changed when CPI data for June was released on July 11th. The unexpectedly good inflation numbers were interpreted very positively by investors – particularly for smaller cap stocks and the interest sensitive sectors which benefit most from lower rates. Many investors reduced their exposure to high-flying tech companies to move into these other areas. See Chart 1.

While lower rates will benefit small-cap companies, the sustainability of the current small-cap rally appears unsustainable so long as their earnings growth remains stagnant while those of the S&P 500 continue to rise. See Chart 2. Furthermore, small-cap indexes may not be able to generate the same returns they have historically. Many of the high growth companies that would have gone public in the past remain private much longer until being acquired by giants like Microsoft and Eli Lilly.

Separately, the artificial intelligence (AI) theme that drove the outsized stock gains in the Magnificent 7 has lost momentum. Investors have very high earnings expectations and are becoming increasingly critical of significant AI investments that show no clear path to future profits. Yet July ended on a strong note of confidence across market sectors.

However, we certainly note the major change in market sentiment as August opened. The weak manufacturing and jobs reports along with just “OK” earnings out of several Magnificent 7 stocks sent many traders to the exits. Stocks across the globe plunged on August 1st and 2nd and continued to decline at the start of the week of August 5th.

Source: The Wall Street Journal

Source: The Wall Street Journal, @The Terminal, Bloomberg Finance L.P.

A cyclical peak in the U.S. stock market at the end of July fits the average seasonality pattern of the market since 1993 and would not be unexpected. See Chart 3.

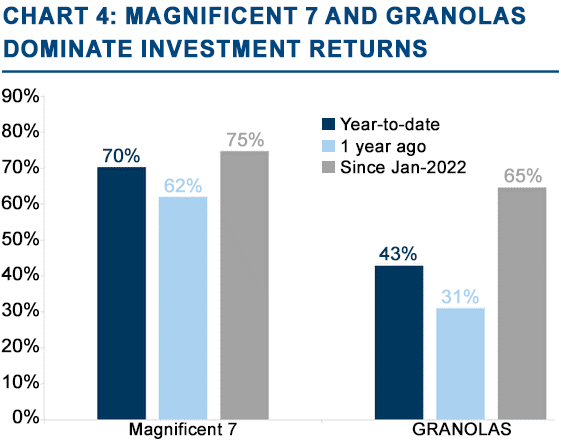

International Stocks. Despite Europe’s anemic economic growth their primary stock index, the STOXX 600, has managed to perform relatively well thanks to a subset of 11 stocks referred to as the “GRANOLAS”, or Europe’s answer to the Magnificent 7.

Chart 4 shows the contribution of the Magnificent 7 to the S&P 500 returns (in various time periods) and the GRANOLAS contribution to the STOXX 600. There is no doubt that large cap growth stocks have driven performance in most major stock indexes in recent years.

Bonds. As mentioned in the Economy section, the continued decline in inflation along with rising unemployment has set the stage for the Fed to begin lowering interest rates. It appears that money market yields above 5% will not survive into 2025.

Bond investors jumped the gun by buying high quality bonds aggressively bringing the yield on the 10-year U.S. Treasury bond down over 60 basis points (0.6%) in just one month to under 4% (3.8% at the close on Friday). Investors are betting the Fed will bring the Fed Funds rate down to at least 3% once they begin to reduce rates. In a recession, the Fed would likely push rates much lower.

Source: The Wall Street Journal

Source: The Wall Street Journal, Goldman Sachs

Real Assets. Most real assets were the biggest winners in July after a lengthy period of underperformance. Some areas of commercial real estate have faced the dual headwinds of high vacancy rates and much higher financing costs. A deterioration in commercial real estate …and its impact on regional banks…continues to be a major risk.

Yet with the prospect of lower interest rates coming soon, many commercial real estate projects should receive a much-needed lifeline. This anticipation led to the sharp rebound in REITs and regional banks in July as investors sought out attractive yields and worried less about the risk of default.

Unfortunately, most commodity producers did not participate in the run up of real asset sectors. It appears that investors see the general slowdown in global economic growth as a growing headwind for these stocks.

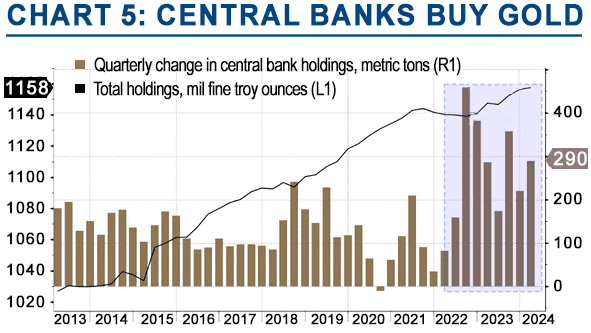

Gold. Gold prices continued to rise in July. As gold and bonds are often seen as competing assets, declining yields provided an added boost for gold. Goldman Sachs recently raised their 2025 price target for gold to $2,700, citing increased demand from China – both consumers and government alike. Gold’s primary driver remains the heightened geopolitical risks along with the enhanced buying by central banks. See Chart 5.

Source: The Wall Street Journal